Six Charts Explain How Workers’ Compensation Is Deteriorating

Six Charts Explain How Workers’ Compensation Is Deteriorating

by Jessica Schieder, 3/30/2015 Click here for full article

Workers’ compensation is a state-based government program that has protected American workers for close to a century. Throughout the early part of U.S. history, injured workers were taken care of by the communities they were a part of: churches, worker’s benevolence associations, neighbors, or extended family. But when workplace deaths and injuries soared during the industrial revolution, government stepped in to help.

Today, workers who are injured on the job or become ill after long-term exposure to workplace hazards are able to collect workers’ compensation. This financial support helps them pay medical bills, offers compensation for lost wages, and provides income to help pay for their living expenses while they are out of work. This mandatory insurance system is designed to provide a safety net for people who suffer harm on the job.

To pay for this program, employers contribute to a state program for the benefit of their employees. Each state sets the rate it charges employers, based on the risk level of a workplace. This rewards and encourages employers with safer workplaces since they pay a lower rate for their employees than workplaces with worse injury rates. States also set the benefit levels paid to injured workers, which vary dramatically across states. Additionally, there is no federal minimum level of benefits that a worker can count on in the event of an accident.

Recent reports paint a picture of a workers’ compensation system that is failing to adequately protect workers.

Employers are paying less into the workers’ compensation system than in years past, and the families of injured workers in many states are receiving less support.

For example, North Dakota employers were paying $2.39 into workers’ comp for every $100 in wages in 1988. By 2014, this amount had fallen to $0.88 – meaning employer contributions to workers’ comp had dropped by more than 60 percent. Over the same period of time, North Dakota increased the standards it requires for workers to qualify for workers’ comp benefits; as a result, the percentage of workers’ claims that were denied increased by 25 percent. North Dakota has been increasingly relying on out-of-state doctors to resolve claim disputes—these doctors rule against the judgment of a patient’s personal doctor most of the time, further reducing benefits.

These six charts explain how workers’ compensation is being eroded today and why the system is increasingly unequal and inadequate.

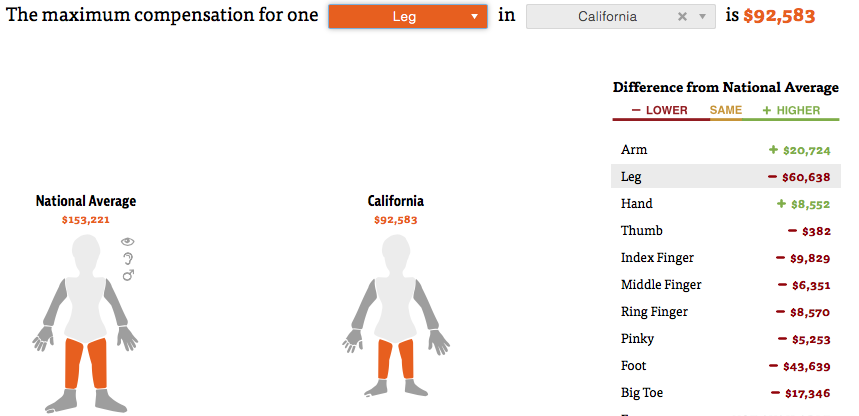

1. Workers’ compensation is surprisingly unequal between states.

There are dramatic disparities between the workers’ compensation benefits injured and ill workers are able to receive in different states, leaving many workers with unequal and inadequate compensation. In investigating the arm amputations of two men on either side of the Alabama-Georgia state line, NPR and ProPublica found a stark difference in the amount of workers’ compensation each worker was eligible to receive over their lifetime. One worker who lived and worked in Alabama received just $45,000 for the loss of his arm, slightly less than the $48,840 maximum lifetime benefit allowed under Alabama law. Less than 75 miles away in Georgia, another worker was awarded benefits that would last his lifetime, potentially totaling more than $740,000 after losing his arm in a similar industrial accident.

To see how a worker in your state would be compensated for the loss of a limb, try out this interactive toolfrom ProPublica.

2. The amount employers pay into workers’ compensation programs is at historic lows.

Businesses are quick to complain that the cost of contributing to workers’ compensation programs are eating into their profits. But the premiums are at historic lows, despite increases in health care costs. In turn, states with stingier worker compensation programs have in recent years marketed themselves as business-friendly to companies looking to cut costs.

See what employers in your state are paying in premiums to support workers’ comp.

3. Workers’ comp is not burdening business.

Nationally, workers’ comp only accounts for 44 cents of the average $31.32 that private employers spend on each worker per hour. This means that the program makes up roughly 1.4 percent of the cost of compensating employees.

4. The costs of workplace injuries and illness have shifted to workers.

Recent changes in workers’ comp at the state level have made it more difficult for injured or ill workers to receive the full benefits they would otherwise be entitled to. In turn, workers’ comp now makes up only about 20 percent of the cost of reported injuries or illnesses. Workers and their families bear at least half of the cost of their injuries, although the real number is likely higher as many injuries go unreported.

Failing to cover the full cost of injuries or illness on the job disproportionately hurts low-income workers. Lower-wage workers are also the least able to absorb the costs of an injury. Because families are unable to shoulder these costs, taxpayers are being asked to take on a greater share of the costs of workplace injuries and illness through public assistance programs like Social Security Disability Insurance.

5. Not all workers are covered by workers’ compensation.

Regulations vary by state, but generally contract workers, temps, and self-employed workers do not qualify for workers’ compensation. Thirteen states also exempt businesses with very small numbers of employees from having to provide workers’ comp benefits. This means these individuals are largely unprotected in the event they are injured or fall ill on the job.

At last count, independent contractors or contingent workers made up 30 percent of the workforce, equal to 42.6 million people. The portion of Americans characterized as freelancers is expected to surpass 40 percent of the workforce by 2020, leaving tens of millions of American workers without access to workers’ comp. Many workers are mischaracterized as independent contractors by their employers in order to reduce labor costs. This practice deprives workers of benefits and puts them outside of many legal protections in order to increase profit margins.

6. The U.S. can do a better job of protecting workers.

The United States has fallen behind other industrialized countries in its efforts to reduce workplace deaths and injury. While the United States has historically been a global leader in workplace safety, budget cuts for the agencies regulating workplace safety, coupled with relaxed standards and more industry self-regulation, have led to U.S. workers facing greater risks than their counterparts in other nations. Countries like the United Kingdom have prioritized workplace safety and worker fatality rates have fallen at a faster rate than in the United States, where fatalities have fallen but less quickly.

The chart below compares the frequency in which workers were killed on the job in the United States, the United Kingdom, and Germany in 2011, the most recent year for which standard European data is available.